.png)

The mortgage industry often discusses change, but most of what passes for analysis is either doom-mongering about affordability or cheerleading about resilience. CMHC's Fall 2025 Residential Mortgage Industry Report cuts through both. The numbers reveal an industry in the middle of a fundamental restructuring, and if you're not paying attention, you're missing where the money is moving.

The Death of the Traditional 5-Year Fixed

Let's start with the headline: Canadian borrowers have essentially given up on 5-year fixed mortgages. Just 17% of new mortgages in August 2025 carried that once-dominant term. Meanwhile, 43% went with 3-to-5 year terms, and variable-rate mortgages that surged in 2024 have reversed course as borrowers sought the certainty of fixed rates at lower prices.

What's driving this? Borrowers are making a calculated bet. They're assuming rates will drop further before renewal, so why lock in for five years when you can grab a lower rate on a shorter term and reassess in 2027 or 2028? It's not irrational. The Bank of Canada has reduced its rate from 5% to 2.25% in just 18 months. Many economists expect rates to settle around 2%, which would put us firmly in stimulative territory.

For brokers and agents, this creates a planning challenge and an opportunity. The challenge: Your clients are building renewal risk into their strategy, which means you need to track those renewal dates more carefully than ever. The opportunity: shorter terms mean more frequent touchpoints and more chances to demonstrate value when those renewals hit.

Big Banks Are Getting Bigger (But Not the Way You Think)

RBC's acquisition of HSBC Canada was completed in March 2024, and the market share data is now finally catching up. The Big 6 banks increased their share of outstanding mortgages by 2.6 percentage points in the first quarter of 2025. That sounds modest until you remember we're talking about a $2.3 trillion market. Small percentage moves represent billions in lending volume.

Here's what matters: HSBC was the rate disruptor. They consistently offered below-market pricing to attract well-qualified customers. Brokers used HSBC rates as leverage in negotiations with other banks. That competitive pressure is now gone, consolidated into RBC's portfolio. The Competition Bureau stated this when it approved the deal, noting HSBC's limited market penetration but acknowledging its role in driving down rates.

The counterbalancing force? Credit unions. They grew originations by 20% year-over-year, with massive jumps in insured refinances (up 103%) and insured switches (up 187%). That growth is being driven by borrowers who are financially tapped out and seeking better terms or cash to consolidate their debt. If you're working with clients in financial distress, credit unions deserve a closer look right now.

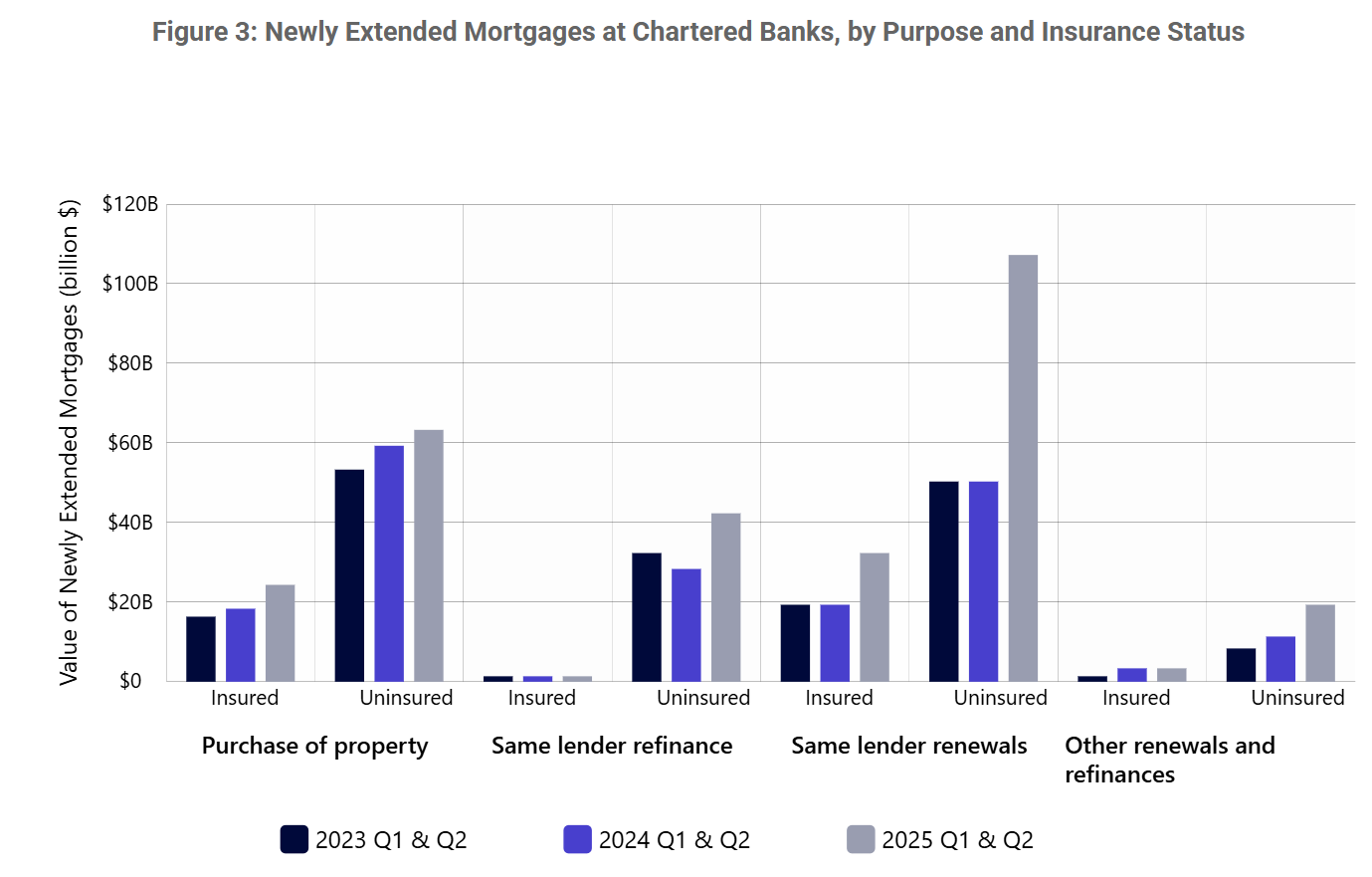

The Renewal Tsunami Is Here

Same-lender renewals at chartered banks more than doubled in H1 2025 compared to H1 2024. This was entirely predictable. The mortgages originated during the 2020-2021 frenzy are reaching their 5-year mark, and all those shorter 2-3 year terms from 2022-2023 are coming due simultaneously.

However, here's the twist: the removal of the stress test for straight renewal switches means borrowers can shop around without the qualification headache that previously kept them from doing so. The data proves it worked. Uninsured lender switches jumped 67% to $19 billion, and interest rates on those renewals dropped 25% compared to just 17% on new mortgages.

Translation: lenders are competing harder for renewal business because they know borrowers can actually leave now. For brokers, this is the gift that keeps on giving. Your existing clients who renewed on short-term contracts (2-3 years ago)? They're coming back around, and they have options. Your job is to make sure they know it.

The Amortization Creep No One Wants to Talk About

Here's the uncomfortable truth buried in CMHC's data: over 60% of new uninsured mortgages now carry amortizations longer than 25 years, and that percentage has held steady for four consecutive quarters even as rates fell and prices stabilized.

Longer amortizations were initially a response to rate shock. But they've become permanent. Borrowers like the lower monthly payment, even though it means paying significantly more interest over the life of the loan and building equity more slowly.

From a risk perspective, longer amortizations increase the likelihood of loss in the event of default because less principal gets repaid. From a client service perspective, you need to have honest conversations about the long-term cost of this convenience.

What This Means Going Forward

The mortgage market is more competitive than it has been in years, notably around renewal periods. The rule changes on insured lending were effective; traditional lenders significantly expanded their business. And borrowers are making strategic decisions about term length based on rate expectations, which means they're paying attention in ways they weren't during the 2020-2021 madness.

For professionals, the opportunity lies in the renewal wave, the flexibility surrounding switching, and the growth occurring at credit unions and alternative lenders that are lending more conservatively but still expanding faster than the national average. The market isn't broken. It's just different. And different creates opportunity for people who adapt.

.png)

.png)

.svg)

.svg)

.svg)